A useful tool for demonstrating certain transactions and events is the T-account. Importantly, one would not use T-accounts for actually maintaining the accounts of a business. Instead, they are just a quick and simple way to figure out how a small number of transactions and events will impact a company. T-accounts would quickly become unwieldy in an enlarged business setting. In essence, T-accounts are just a “scratch pad” for account analysis. They are useful communication devices to discuss, illustrate, and think about the impact of transactions. The physical shape of a T-account is a “T,” and debits are on the left and credits on the right. The “balance” is the amount by which debits exceed credits (or vice versa).

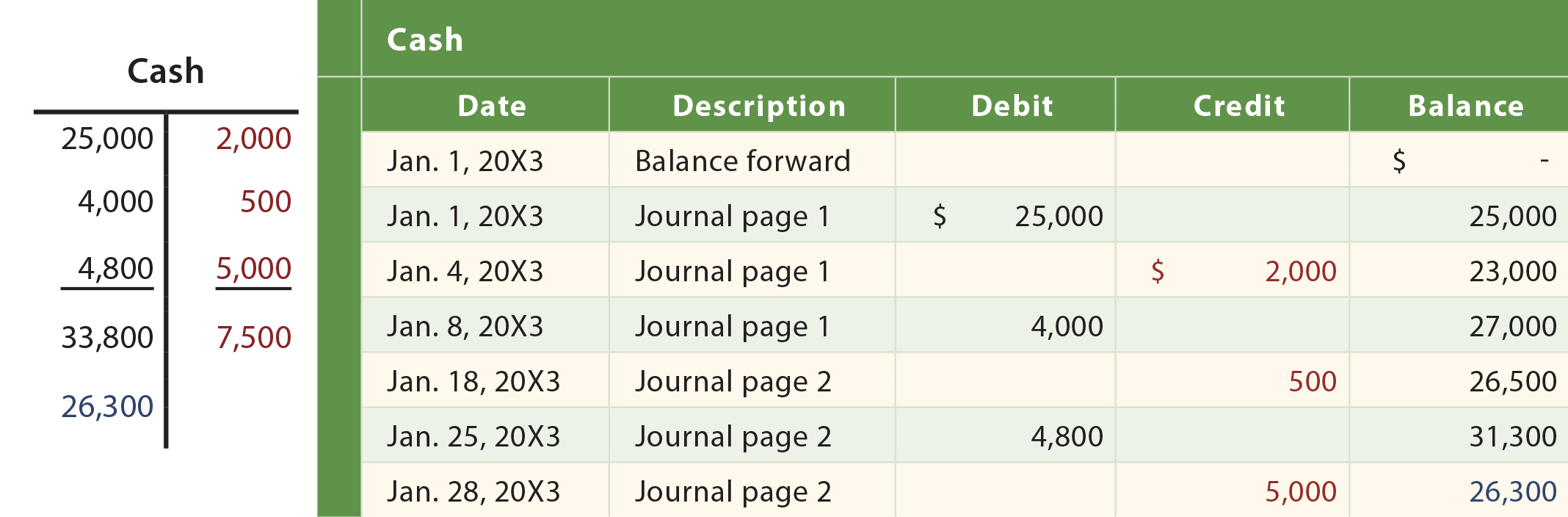

Below is the T-account for Cash for the transactions and events of Xao Corporation. Carefully compare this T-account to the actual running balance ledger account which is also shown (notice that the debits in black total to $33,800, the credits in red total to $7,500, and the excess of debits over credits is $26,300 — which is the resulting account balance shown in blue).

Need help preparing for an exam?

Check out ExamCram the exam preparation tool!

| Did you learn? |

|---|

| Know what a T-account is and how it can be used. |

| Be able to prepare a T-account that corresponds to a general ledger account. |