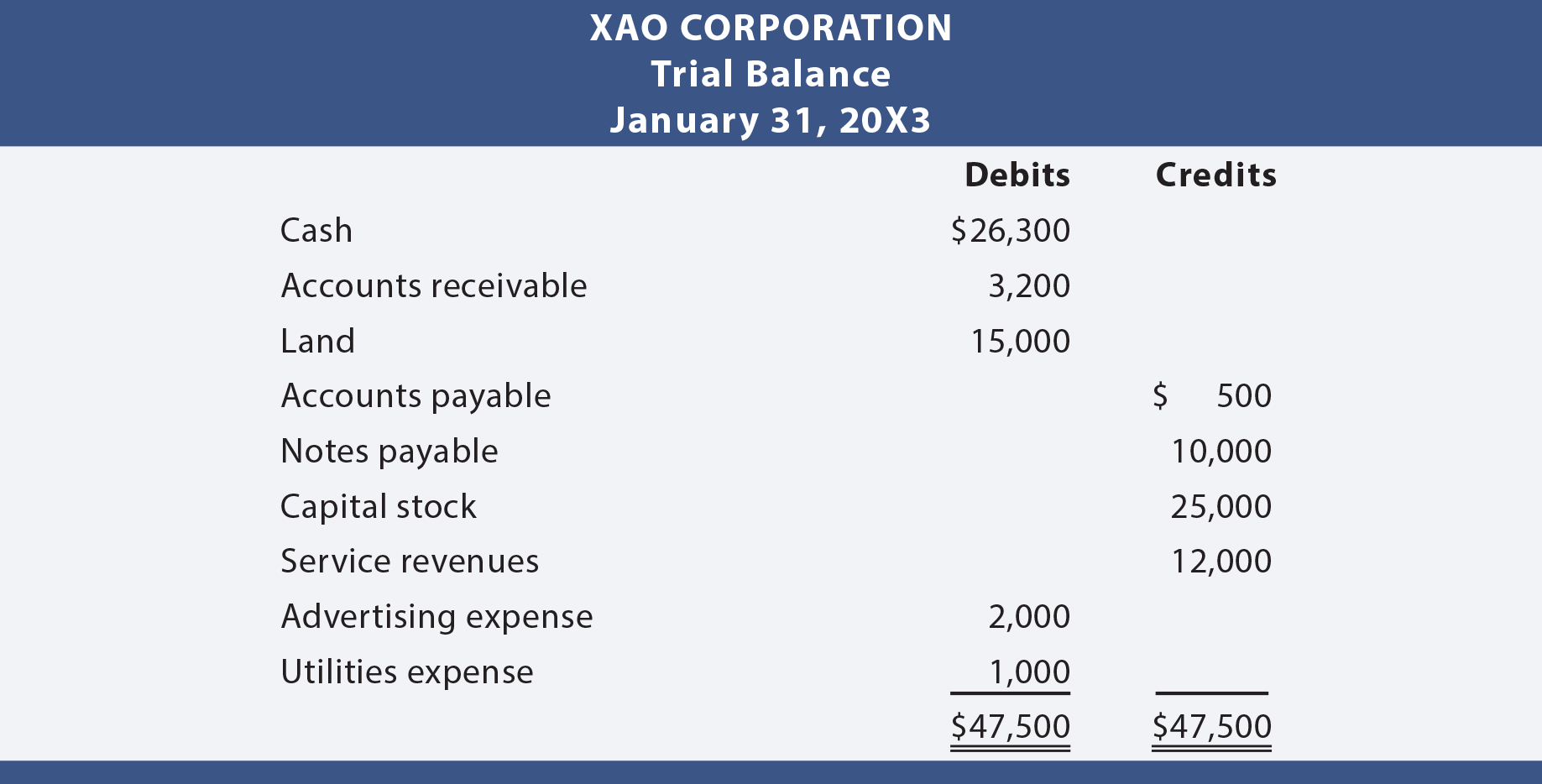

After all transactions have been posted from the journal to the ledger, it is a good practice to prepare a trial balance. A trial balance is simply a listing of the ledger accounts along with their respective debit or credit balances. The trial balance is not a formal financial statement, but rather a self-check to determine that debits equal credits. Following is the trial balance prepared for Xao Corporation.

Debits Equal Credits

Since each transaction was journalized in a way that insured that debits equaled credits, one would expect that this equality would be maintained throughout the ledger and trial balance. If the trial balance fails to balance, an error has occurred and must be located. It is much better to be careful as one proceeds, rather than having to go back and locate an error after the fact. Be aware that a “balanced” trial balance is no guarantee of correctness. For example, failing to record a transaction, recording the same transaction twice, or posting an amount to the wrong account would produce a balanced (but incorrect) trial balance.

Financial Statements From The Trial Balance

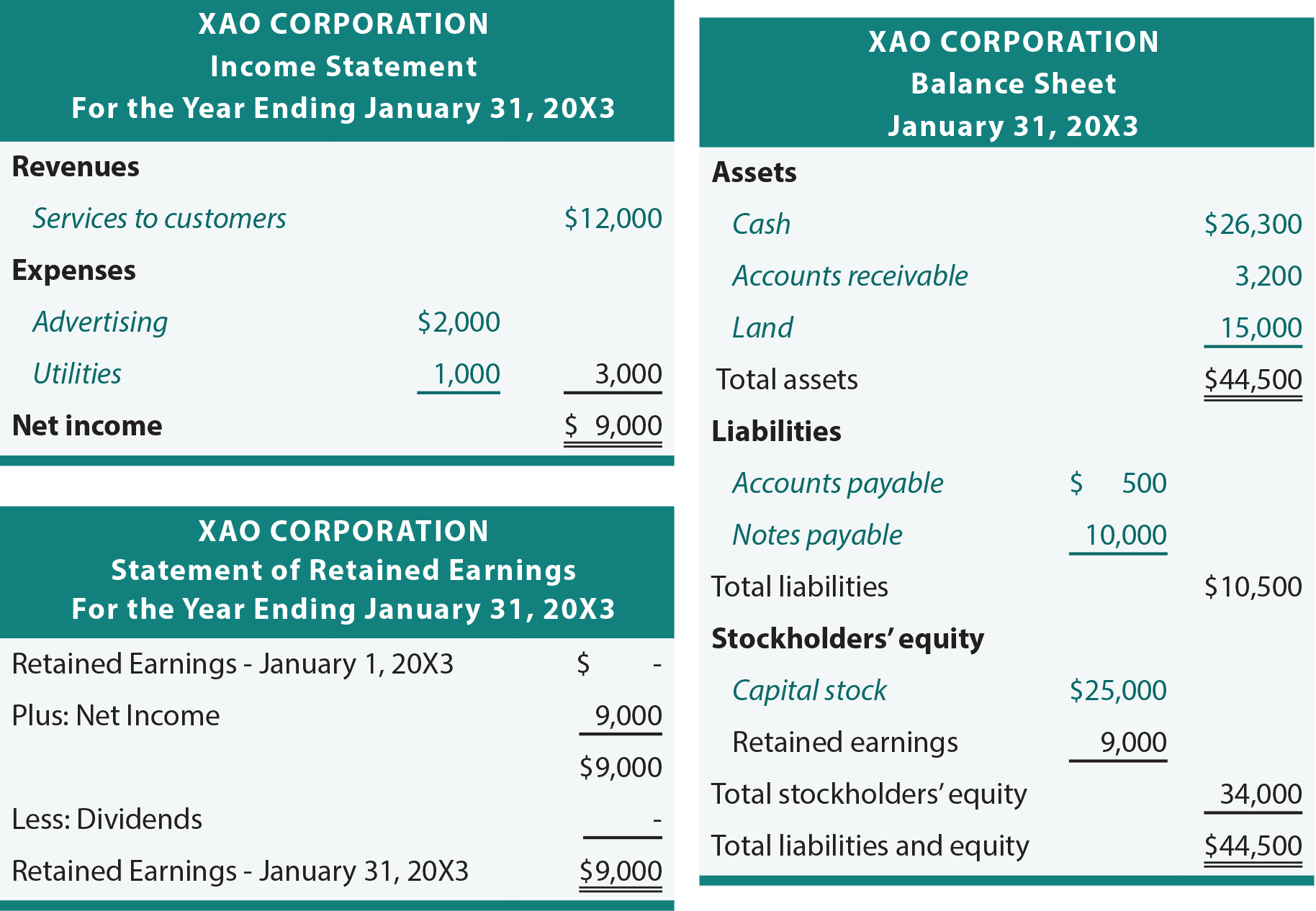

The next chapter reveals additional adjustments that may be needed to prepare a truly correct and up-to-date set of financial statements. But, for now, a tentative set of financial statements could be prepared based on the trial balance. The basic process is to transfer amounts from the general ledger to the trial balance, then into the financial statements:

In reviewing the following financial statements for Xao, notice that italics are used to draw attention to the items taken directly from the previously shown trial balance. The other line items and amounts simply relate to totals and derived amounts within the statements.

Chart of Accounts

A listing of all accounts in use by a particular company is called the chart of accounts. Individual accounts are often given a specific reference number. The numbering scheme helps keep up with the accounts in use and the classification of accounts. For example, all assets may begin with “1” (e.g., 101 for Cash, 102 for Accounts Receivable, etc.), liabilities with “2,” and so forth. The assignment of a numerical value to each account assists in data management, in much the same way as zip codes help move mail more efficiently. Many computerized systems allow rapid entry of accounts by reference number rather than by entering a full account description. A simple chart of accounts for Xao Corporation might appear as follows:

- No. 101: Cash

- No. 102: Accounts Receivable

- No. 103: Land

- No. 201: Accounts Payable

- No. 202: Notes Payable

- No. 301: Capital Stock

- No. 401: Service Revenue

- No. 501: Advertising Expense

- No. 502: Utilities Expense

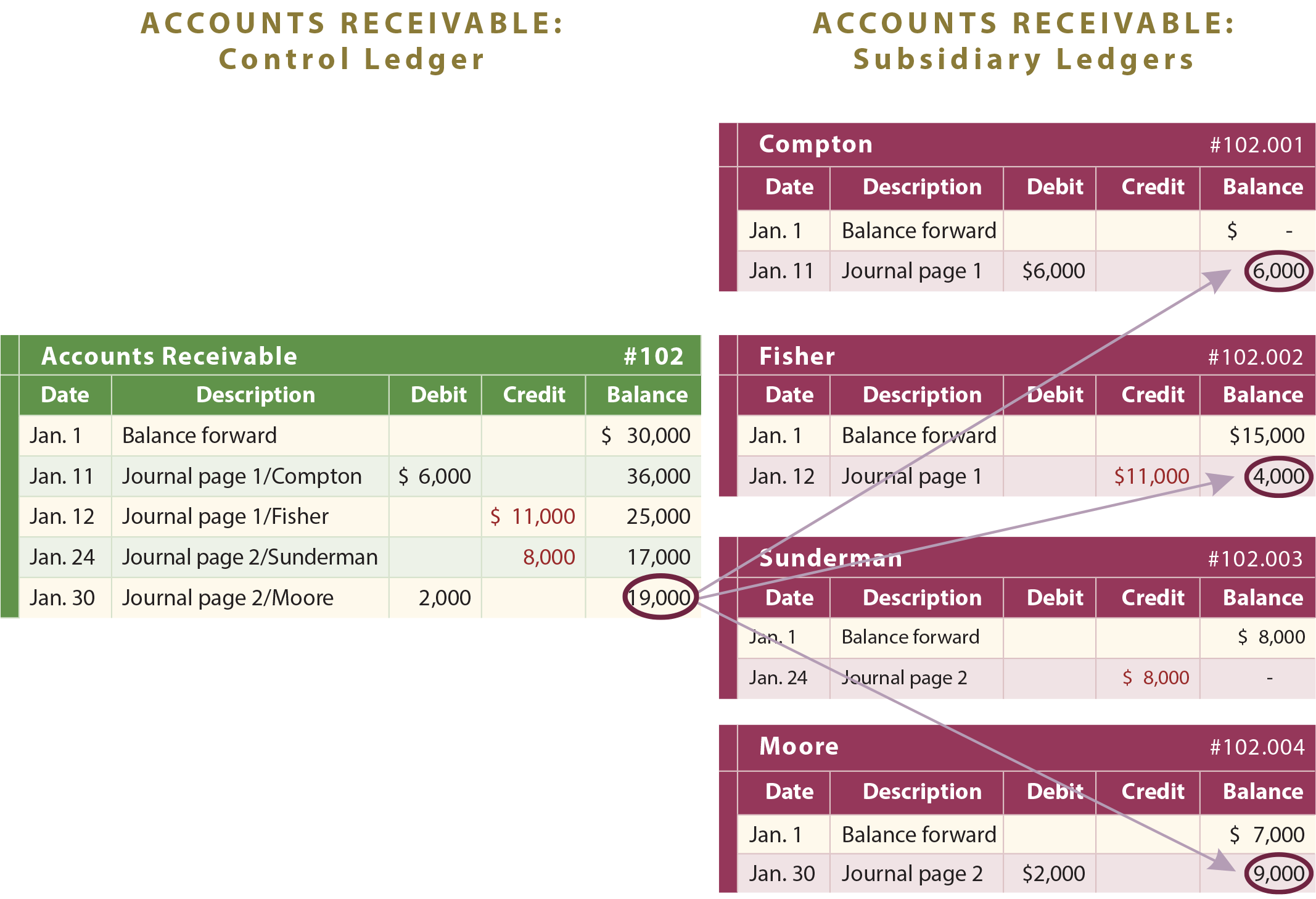

Another benefit is that each account can be further subdivided into subsets. For instance, if Accounts Receivable bears the account number 102, one would expect to find that individual customers might be numbered as 102.001, 102.002, 102.003, etc. This facilitates the maintenance of “subsidiary” account records which are the subject of the next section of this chapter.

Control and Subsidiary Accounts

Some general ledger accounts are made of many sub-components. For instance, a company may have total accounts receivable of $19,000, consisting of amounts due from Compton, Fisher, and Moore. The accounting system must be sufficient to reveal the total receivables, as well as amounts due from each customer. Therefore, sub-accounts are used. In addition to the regular general ledger account, separate auxiliary receivable accounts would be maintained for each customer, as shown in the following detailed illustration:

The total receivables are the sum of all the individual receivable amounts. Thus, the Accounts Receivable general ledger account total is said to be the control account or control ledger, as it represents the total of all individual subsidiary account balances. It is simply imperative that a company be able to reconcile subsidiary accounts to the broader control account that is found in the general ledger. Here, computers can be particularly helpful in maintaining the detailed and aggregated data in perfect harmony.

Need help preparing for an exam?

Check out ExamCram the exam preparation tool!

| Did you learn? |

|---|

| What is the purpose of a trial balance? |

| Outline the accounting steps that lead to the preparation of a trial balance. |

| If a trial balance is in balance, is it necessarily correct? |

| Know how a trial balance can be used to facilitate preparation of financial statements. |

| Will a trial balance necessarily produce correct financial statements? |

| Be able to explain what a chart of accounts is and how it is used. |

| Describe the nature and purpose of control and subsidiary accounts. |