Whether a company uses a periodic or perpetual inventory system, a physical inventory (i.e., physical count) of goods on hand should occur from time to time. The quantities determined via the physical count are presumed to be correct, and any differences should result in an adjustment of the accounting records. Sometimes, however, a physical count may not be possible or is not cost effective, and estimates are employed.

Gross Profit Method

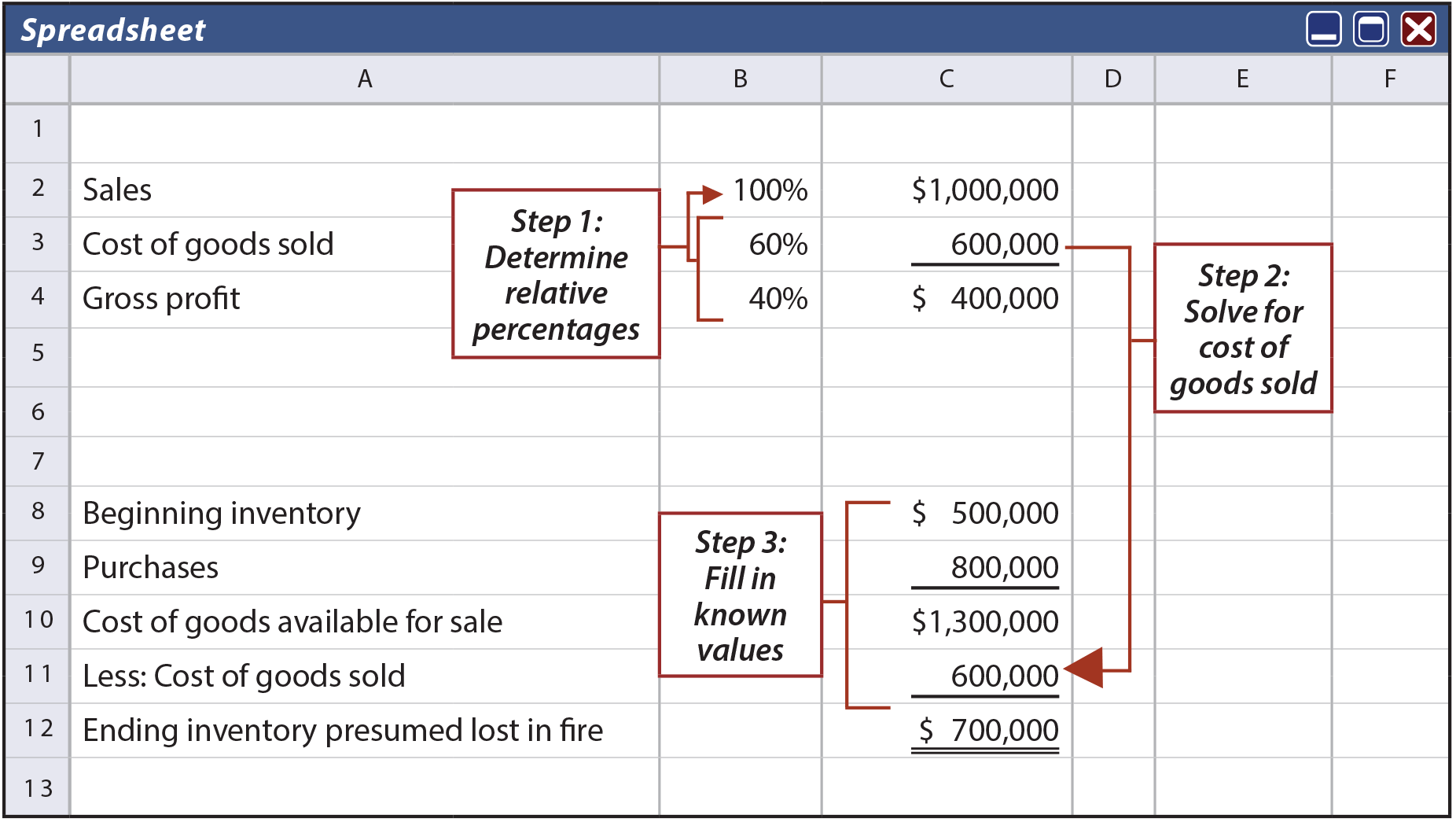

One such estimation technique is the gross profit method. This method might be used to estimate inventory on hand for purposes of preparing monthly or quarterly financial statements, and certainly would come into play if a fire or other catastrophe destroyed the inventory. Very simply, a company’s normal gross profit rate (i.e., gross profit as a percentage of sales) would be used to estimate the amount of gross profit and cost of sales. Assume that Tiki’s inventory was destroyed by fire. Sales for the year, prior to the date of the fire were $1,000,000, and Tiki usually sells goods at a 40% gross profit rate. Therefore, Tiki can readily estimate that cost of goods sold was $600,000. Tiki’s beginning of year inventory was $500,000, and $800,000 in purchases had occurred prior to the date of the fire. The inventory destroyed by fire can be estimated via the gross profit method, as shown.

Retail Method

A method that is widely used by merchandising firms to value or estimate ending inventory is the retail method. This method would only work where a category of inventory has a consistent mark-up. The cost-to-retail percentage is multiplied times ending inventory at retail. Ending inventory at retail can be determined by a physical count of goods on hand, at their retail value. Or, sales might be subtracted from goods available for sale at retail.

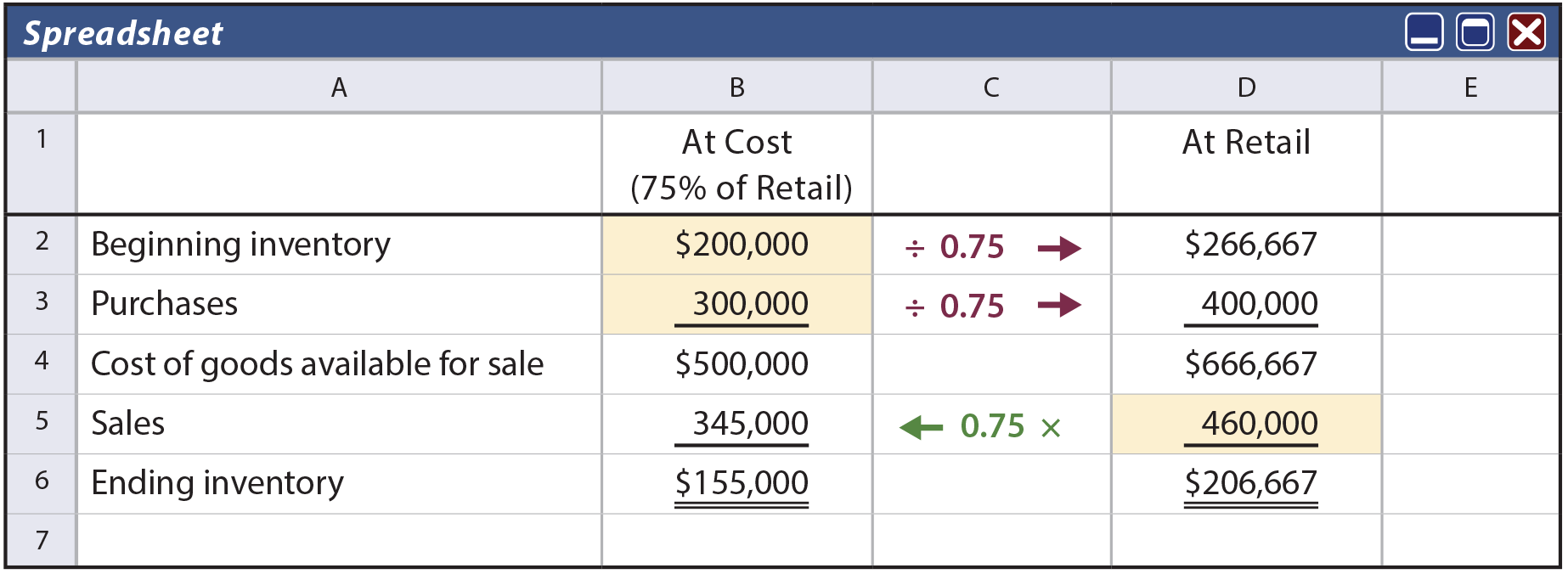

Crock Buster sells pots that cost $7.50 for $10. This yields a cost-to-retail percentage of 75%. The beginning inventory totaled $200,000 (at cost), purchases were $300,000 (at cost), and sales totaled $460,000 (at retail).

The only”givens”are highlighted in yellow. These three data points are manipulated by the cost-to-retail percentage to solve for ending inventory cost of $155,000. Be careful to note when the percentage factors are divided and when they are multiplied.

Need help preparing for an exam?

Check out ExamCram the exam preparation tool!

| Did you learn? |

|---|

| Understand the occasional need for inventory estimates. |

| Be able to apply the gross profit method. |

| Understand the benefits and application of the retail inventory method. |