Understand that international trade no longer simply means importing and exporting. Companies have added subsidiaries in many countries, formed cooperative alliances, listed shares on multiple stock exchanges around the globe, engaged in global cross-border debt financing, and set up service centers that utilize technology to provide seamless customer support around the world.

Understand that international trade no longer simply means importing and exporting. Companies have added subsidiaries in many countries, formed cooperative alliances, listed shares on multiple stock exchanges around the globe, engaged in global cross-border debt financing, and set up service centers that utilize technology to provide seamless customer support around the world.

Companies engaging in global business face some specific reporting challenges. Two of those challenges are (1) how to consolidate global subsidiaries and (2) how to account for global transactions denominated in alternative currencies.

Global Subs

When a parent corporation has a subsidiary outside of its home country, the financial statements of that subsidiary may be prepared in the “local” currency of the country in which it operates. But, the parent’s financials are prepared in the “reporting” currency of the country in which it is domiciled. Thus, to consolidate the parent and sub first requires converting the sub’s financial information into the reporting currency. Facts and circumstances will dictate whether the conversion process occurs by a process known as the functional currency translation approach or an alternative approach known as remeasurement.

Global Trading

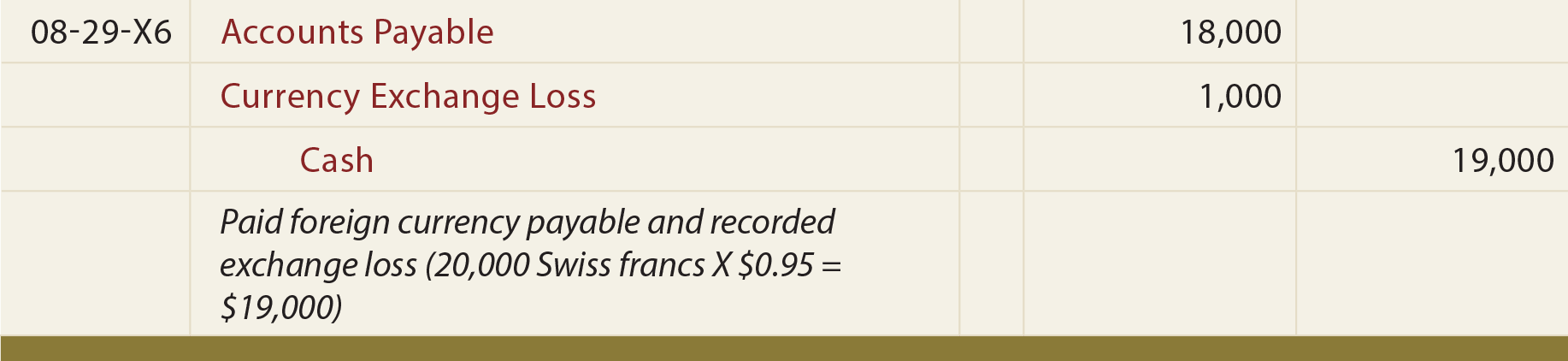

Many firms buy goods from foreign suppliers and/or sell goods to foreign customers. The terms of the transaction will stipulate how payment is to occur and the currency for making settlement. If the currency is “foreign,” then some additional thought must be given to the bookkeeping. Suppose Bentley’s Bike Shop purchases bicycles from GiroCycle of Switzerland. On July 1, 20X6, Bentley purchased bicycles, agreeing to pay 20,000 Swiss francs within 60 days. Bentley is in Cleveland, Ohio, and the U.S. dollar is its primary currency. On July 1, Bentley will record the purchase by debiting Inventory and crediting Accounts Payable. But, what amount should be debited and credited? If 20,000 were used, the accounts would cease to be logical. The total Inventory balance would be illogical since it would include this item, and all other transactions in other currencies. Total Accounts Payable would become unintelligible as well. Therefore, Bentley needs to measure the transaction in dollars. On July 1, assume that the current exchange rate (i.e., the “spot rate”) is 0.90 U.S. dollars to acquire 1 Swiss franc. The correct entry would be:

By the August 29 settlement date, assume that the dollar has weakened and the spot rate is $0.95. Bentley will have to pay $19,000 (20,000 X $0.95) to buy the 20,000 francs needed to settle the obligation. The following entry shows that the difference between the initially recorded payable ($18,000) and the cash settlement amount ($19,000) is to be recorded as a foreign currency transaction loss:

If the exchange rate had gone the other way, a foreign currency transaction gain (credit) would have been needed to balance the payable and required cash disbursement.

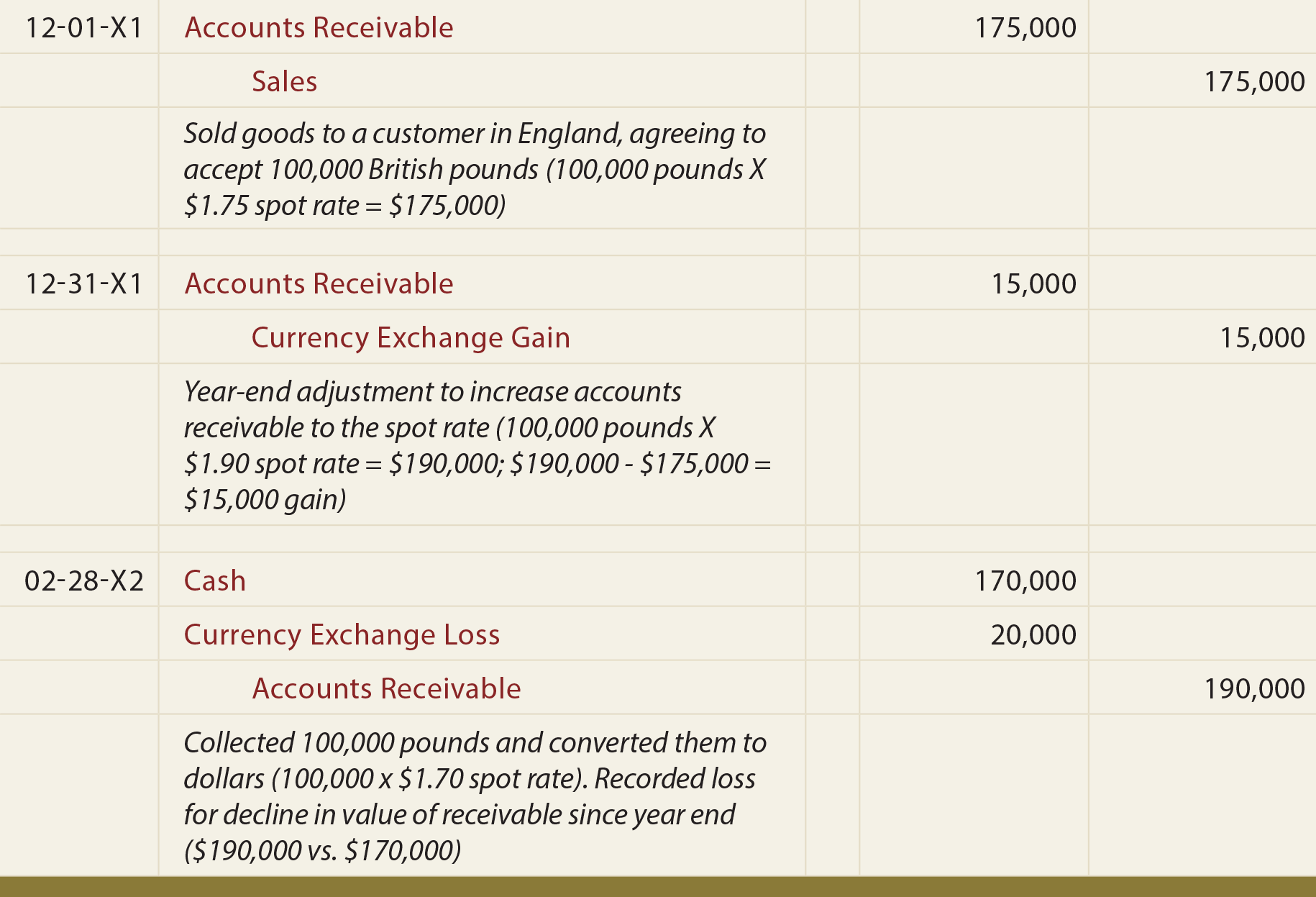

It is important to know that foreign currency payables and receivables that exist at the close of an accounting period must also be adjusted to reflect the spot rate on the balance sheet date. Suppose Vigeland Corporation sold goods to a customer in England, agreeing to accept payment of 100,000 British pounds in 90 days. On the date of sale, December 1, 20X1, the spot rate for the pound was $1.75. Vigeland prepared financial statements at its year end on December 31, 20X1, at which time the spot rate for the pound was $1.90. The foreign currency receivable was collected on February 28, 20X2, and Vigeland immediately converted the 100,000 pounds to dollars at the then current exchange rate of $1.70. The following illustrates Vigeland’s sale, year-end adjustment, and subsequent collection:

Some companies may wish to avoid foreign currency exchange risks like those just illustrated. The simplest way is to convince a trading partner to make or take payment in the home currency. In the alternative, various financial agreements can be structured with banks or others to hedge this risk.

| Did you learn? |

|---|

| What are two key accounting issues that can arise from global commerce? |

| Distinguish between translation and remeasurement, and to what subject do they relate? |

| Know how to account for typical foreign currency transactions, with special attention to appropriate year-end adjustments. |