A comprehensive budget usually involves all segments of a business. As a result, representatives from each unit are typically included throughout the process. The process is likely to be lead by a budget committee consisting of senior-level personnel. Such individuals bring valuable insights about all aspects of sales, production, financing, and other phases of operations. Not only are these individuals ideally positioned to provide the best possible information relative to their respective units, but they are also needed to effectively advocate for the opportunities and resource needs within their unit.

A comprehensive budget usually involves all segments of a business. As a result, representatives from each unit are typically included throughout the process. The process is likely to be lead by a budget committee consisting of senior-level personnel. Such individuals bring valuable insights about all aspects of sales, production, financing, and other phases of operations. Not only are these individuals ideally positioned to provide the best possible information relative to their respective units, but they are also needed to effectively advocate for the opportunities and resource needs within their unit.

The budget committee’s work is not necessarily complete once the budget document is prepared and approved. A remaining responsibility for many committees is to continually monitor progress against the budget and potentially recommend mid-course corrections. The budget committee’s decisions can greatly impact the fate of specific business units, in terms of resources made available as well as setting the benchmarks that will be used to assess performance. As a result, members of the budget committee will generally take their task very seriously.

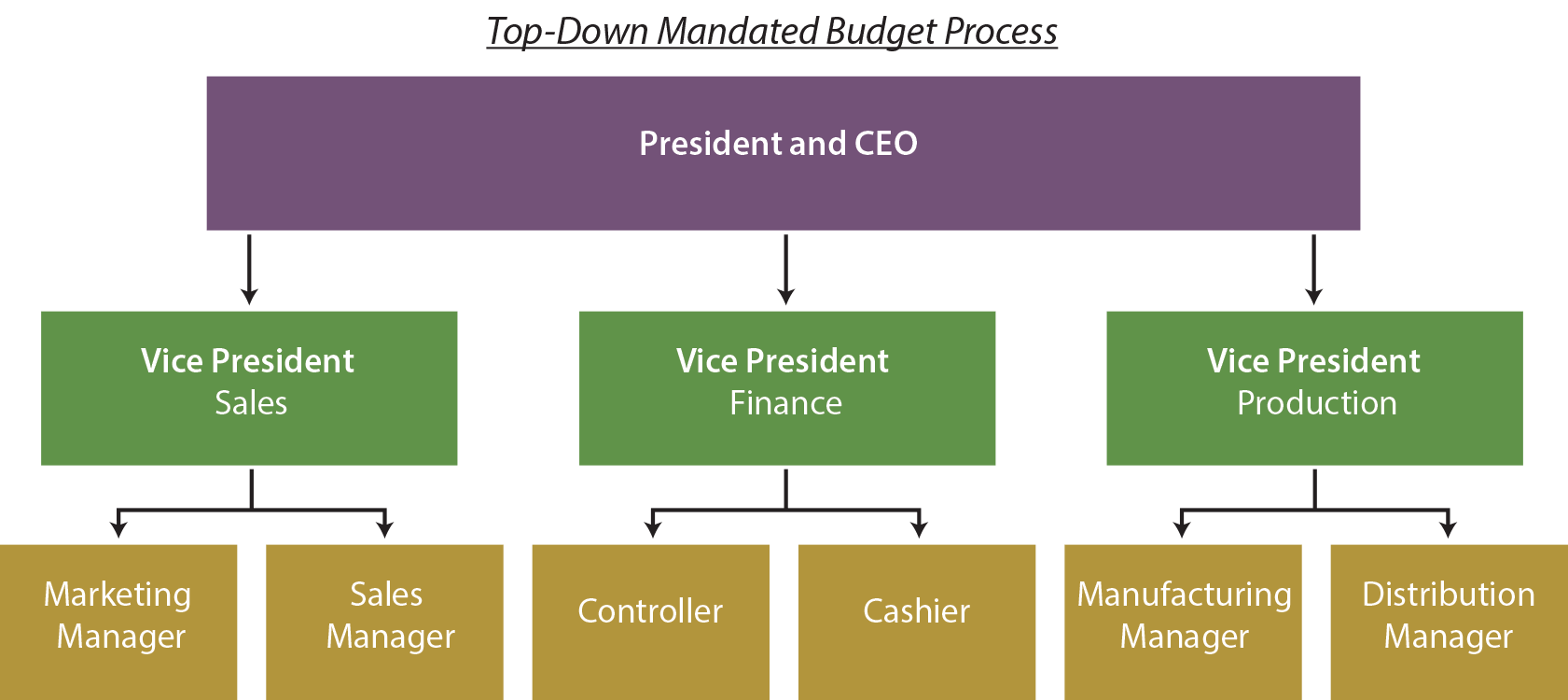

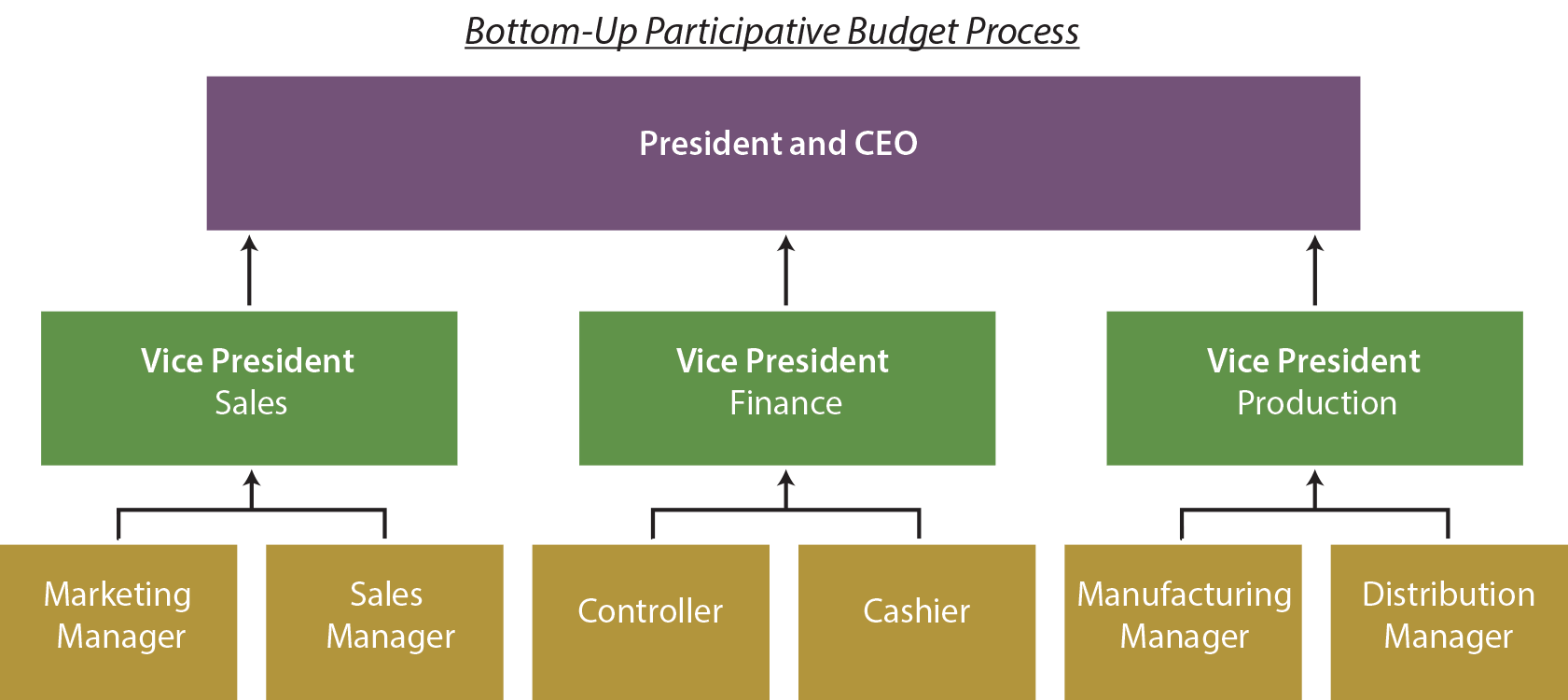

The budget construction process will normally follow the organizational chart. Each component of the entity will be involved in preparing budget information relative to its unit. This information is successively compiled together as it is passed through the organization until an overall budget plan is achieved. But, beyond the data compilation, there is a critical difference in how budgets are actually developed among different organizations. Some entities follow a top-down, or mandated approach. Others utilize a bottom-up, or participative philosophy.

Top-Down Budget

Some entities will follow a top-down mandated approach to budgeting. These budgets will begin with upper-level management establishing parameters under which the budget is to be prepared. These parameters can be general or specific. They can cover sales goals, expenditure levels, guidelines for compensation, and more. Lower-level personnel have very little input in setting the overall goals of the organization. The upper-level executives call the shots, and lower-level units are essentially reduced to doing the basic budget calculations consistent with directives. Mid-level executives may unite the budget process by refining the leadership directives as the budget information is passed down through the organization.

One disadvantage of the top-down approach is that lower-level managers may view the budget as a dictatorial standard. Resentment can be fostered in such an environment. Further, such budgets can sometimes provide ethical challenges, as lower-level managers may find themselves put in a position of ever-reaching to attain unrealistic targets for their units.

On the positive side, top-down budgets can set a tone for the organization. They signal expected sales and production activity that the organization is supposed to reach. Some of the most efficient and successful organizations have a hallmark strategy of being “lean and mean.” The budget is a most effective communication device in getting employees to hear the message and perform accordingly.

Bottom-Up Budget

The bottom-up participative approach is driven by involving lower-level employees in the budget development process. Top management may initiate the budget process with general budget guidelines, but it is the lower-level units that drive the development of budgets for their units. These individual budgets are then grouped and regrouped to form a divisional budget with mid-level executives adding their input along the way.

Eventually top management and the budget committee will receive the overall plan. As one might suspect, the budget committee must then review the budget components for consistency and coordination. This may require several iterations of passing the budget back down the ladder for revision by lower units. Ultimately, a final budget is reached.

The participative budget approach is viewed as self-imposed. As a result, it is argued that it improves employee morale and job satisfaction. It fosters the “team-based” management philosophy that has proven to be very effective for modern organizations. Furthermore, the budget is prepared by those who have the best knowledge of their own specific areas of operation. This should allow for a more accurate budget.

On the negative side, a bottom-up approach is generally more time-consuming and expensive to develop and administer. This occurs because of the repetitious process needed for its development and coordination. Another potential shortcoming has to do with the fact that some managers may try to “pad” their budget, giving them more room for mistakes and inefficiency.

Data Flow

It is very important for managers at all levels to understand how data are transformed as it passes through an organization. As budget information is transferred up and down an organization, the “message” will inevitably be influenced by the beliefs and preferences of the communicators. There is always a chance that information can be transformed and lose its original intent. Top management can lose touch with information originating on the front line, and front-line employees may not always get a clear picture of the goals and objectives originating with senior management.

It is very important for managers at all levels to understand how data are transformed as it passes through an organization. As budget information is transferred up and down an organization, the “message” will inevitably be influenced by the beliefs and preferences of the communicators. There is always a chance that information can be transformed and lose its original intent. Top management can lose touch with information originating on the front line, and front-line employees may not always get a clear picture of the goals and objectives originating with senior management.

There are staggering differences in the organization charts of different entities. Business growth is a natural incubator for expansion of the number of levels within an organization; as a result, great care must be taken to preserve the efficiency and effectiveness of growing entities. Sometimes the very attributes that contribute to growth can be undone by the growth itself. The charts of some entities consume many pages and involve potentially dozens of “levels.” Other companies may have worked to “flatten” their organizational chart to minimize the number of links in the chain of command.

While these endeavors are often seen as attempts to reduce the cost of middle-level management, the overriding issue is to allow top management more clear and direct access to vital information originating with front-line employees (and vice versa). In addition to focusing on revenues and costs, the budget process should also be taken as an opportunity for continuous monitoring of the organizational structure of an entity.

Budget Estimation

Budgets involve a good deal of forward-looking projection. As a result, a certain amount of error is inevitable. Accordingly, it is easy to slip into a trap of becoming inattentive about the estimates that form the basis for a budget. This should be avoided.

Budget estimates should be given careful consideration. They should have a basis in reason and logically be expected to occur. Haphazardness should be replaced by study and statistical evaluation of historical information, as this provides a good starting point for predictions. Changing economic conditions and trends need to be carefully evaluated.

Because budgets frequently form an important part of performance evaluation, human behavior suggests that participants in the budget process are going to try to create “breathing room” for themselves by overestimating expenses and underestimating sales.

Because budgets frequently form an important part of performance evaluation, human behavior suggests that participants in the budget process are going to try to create “breathing room” for themselves by overestimating expenses and underestimating sales.

This deliberate effort to affect the budget is known as creating budget slack or “padding the budget.” This is done in an attempt to create an environment where budgeted goals are met or exceeded. However, this does little to advance the goals of the organization.

When slack is introduced into a budget, employees may fail to maximize sales and minimize costs. For example, once it is clear that budgeted sales goals will be met, there may be a reduction in incentive to push ahead. In fact, there may be some concern about beating sales goals within a period for fear that a new higher benchmark will be established that must be exceeded in a subsequent period. This can result in a natural desire to push pending transactions to future periods. Likewise, padding the planned level of expenses can actually provide incentive to overspend, as managers fear losing money in subsequent budgets if they don’t spend all of the currently budgeted funds. This has the undesirable consequence of encouraging waste.

Zero-Based Budgeting

The problem of budgetary slack is particularly acute when the prior year’s budget is used as the starting point for preparing the current budget. This is called incremental budgeting. It is presumed that established levels from previous budgets are an acceptable baseline, and changes are made based on new information. This usually means that budgeted amounts are incrementally increased. The alternative to incremental budgeting is called “zero-based budgeting.”

With zero-based budgeting, each expenditure item must be justified for the new budget period. No expenditure is presumed to be acceptable simply because it is reflective of the status quo. This approach may have its genesis in governmental units that struggle to control costs. Governmental units usually do not face a market test; they rarely fail to exist if they do not perform with optimum efficiency. Instead, governmental entities tend to sustain their existence by passing along costs in the form of mandatory taxes and fees. This gives rise to considerable frustration in trying to control spending. Some governmental leaders push for zero-based budgeting concepts in an attempt to filter necessary services from those that simply evolve under the incremental budgeting process. Business entities may also utilize zero-based budgeting concepts to reexamine every expenditure during each budget cycle.

With zero-based budgeting, each expenditure item must be justified for the new budget period. No expenditure is presumed to be acceptable simply because it is reflective of the status quo. This approach may have its genesis in governmental units that struggle to control costs. Governmental units usually do not face a market test; they rarely fail to exist if they do not perform with optimum efficiency. Instead, governmental entities tend to sustain their existence by passing along costs in the form of mandatory taxes and fees. This gives rise to considerable frustration in trying to control spending. Some governmental leaders push for zero-based budgeting concepts in an attempt to filter necessary services from those that simply evolve under the incremental budgeting process. Business entities may also utilize zero-based budgeting concepts to reexamine every expenditure during each budget cycle.

While this is good in theory, zero-based budgeting can become very time-consuming and expensive to implement. In business, the opportunity for gross inefficiency is kept in check by market forces, and there may not be sufficient savings to offset the cost of a serious zero-based budgeting exercise. Nevertheless, business managers should be familiar with zero-based budgeting concepts as one tool to identify and weed out budgetary slack. There is nothing to suggest that every unit must engage in zero-based budgeting every year. Instead, a rolling schedule that thoroughly reexamines each unit once every few years may provide a cost-effective alternative.

The Impossible Budget

At the opposite end of budgetary slack is the phenomenon of unattainable budget standards. If employees feel that budgets are not possibly achievable, they may become frustrated or disenchanted. Such a condition may actually reduce employee performance and morale. Good managers should be as alert to this problem as they are to budgetary slack. Suffice it to say that preparing a budget involves more than just number crunching; there is a fair amount of organizational psychology that a good manager must take into account in the process.

Ethical Challenges

Investors often press management to provide forward-looking earnings guidance. Many financial reporting frauds have their origin in overly optimistic budgets and forecasts that subsequently lead to an environment of “cooking the books” to reach unrealistic goals. These events usually start small, with the expectation that time will make up for a temporary problem. The initial seemingly harmless act is frequently followed by an ever-escalating pattern of deception that ultimately leads to collapse.

Investors often press management to provide forward-looking earnings guidance. Many financial reporting frauds have their origin in overly optimistic budgets and forecasts that subsequently lead to an environment of “cooking the books” to reach unrealistic goals. These events usually start small, with the expectation that time will make up for a temporary problem. The initial seemingly harmless act is frequently followed by an ever-escalating pattern of deception that ultimately leads to collapse.

To maintain organizational integrity, senior-level managers need to be careful to provide realistic budget directives. Lower-level managers need to be truthful in reporting “bad news” relative to performance against a budget, even if they find fault with the budget guidelines. All too often, the carnage that follows a business collapse will be marked by management claims that they were misled by lower-level employees who hid the truth. And, lower-level employees will claim that they were pressured by management to hide the truth.

| Did you learn? |

|---|

| Who ordinarily serves on a budget committee and what roles does this group play? |

| Distinguish between the mandated top-down and participative bottom-up budget construction processes. |

| Discuss the nature of budgetary slack. |

| How does the form of organizational structure influence business budgeting, planning, and information flow? |

| Distinguish between incremental and zero-based budgeting approaches. |

| Generally describe potential human behavior and ethical aspects of budgeting. |