The previous chapter provided a comprehensive budget illustration using a static budget. The static budget is one that is developed for a single level of activity. It is very useful for planning and control purposes.

The previous chapter provided a comprehensive budget illustration using a static budget. The static budget is one that is developed for a single level of activity. It is very useful for planning and control purposes.

However, there is a potential shortcoming in using static budgets for performance evaluation. Specifically, when the actual output varies from the anticipated level, variances are likely to arise. These variances can be quite misleading.

The genesis of the problem is that variable costs will tend to track volume. If the company produces and sells more products than anticipated, one would expect to see more variable costs (and vice versa). Presumably, it is a good thing to produce and sell more than planned, but the variances resulting from the higher costs can appear as a bad thing! The opposite occurs when volume is less than anticipated.

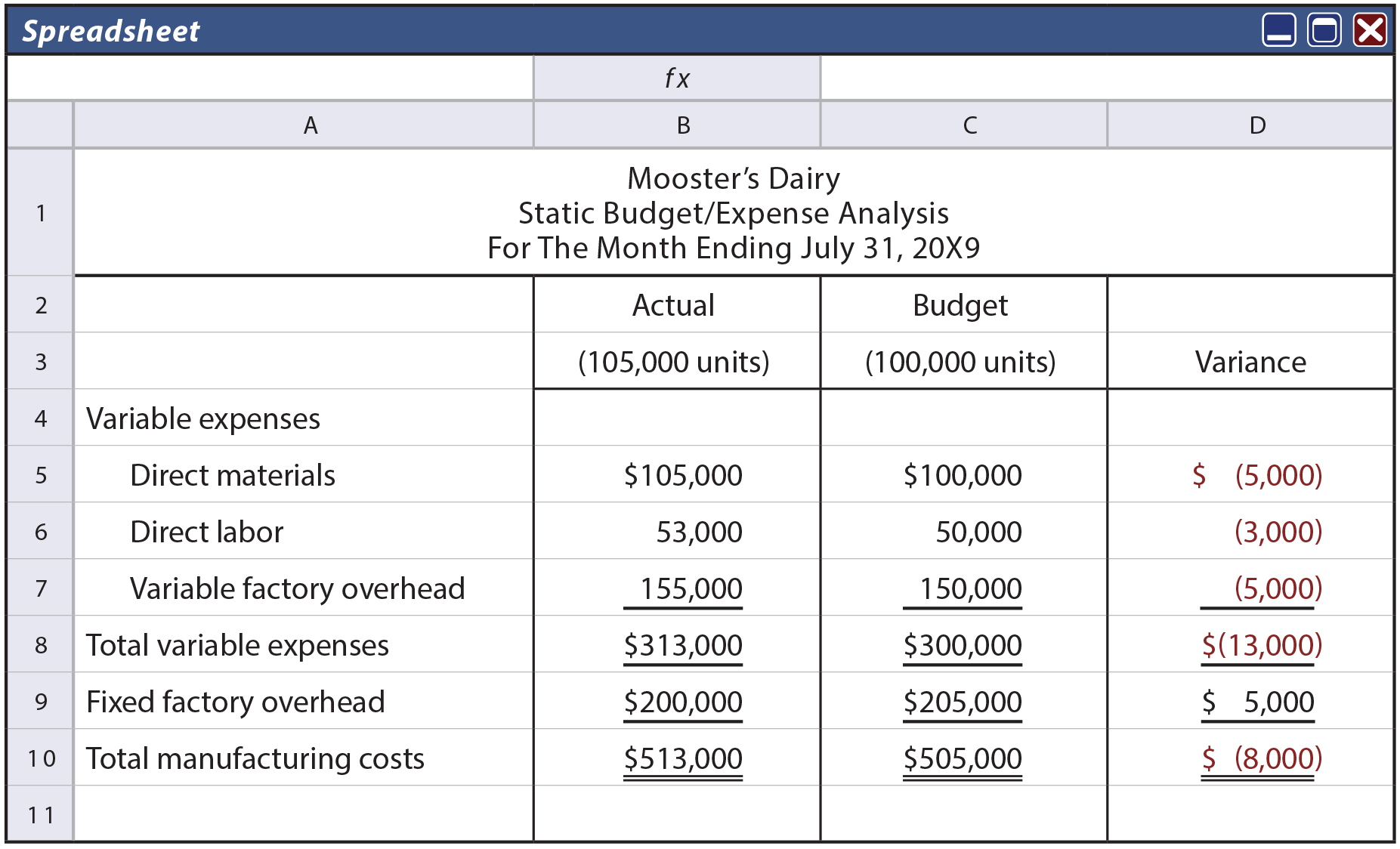

To illustrate, assume that Mooster’s Dairy produces a premium brand of ice cream. Mooster’s Dairy uses a static budget based on anticipated production of 100,000 gallons per month. Cost behavior analysis revealed that direct materials are variable and anticipated to be $1 per gallon ($100,000 in total), direct labor is variable and anticipated to be $0.50 per gallon ($50,000 in total), and variable factory overhead is expected to be $1.50 per gallon ($150,000 in total). Fixed factory overhead is planned at $205,000 per month. The monthly budget for total manufacturing costs is $505,000, as shown in the budget column below.

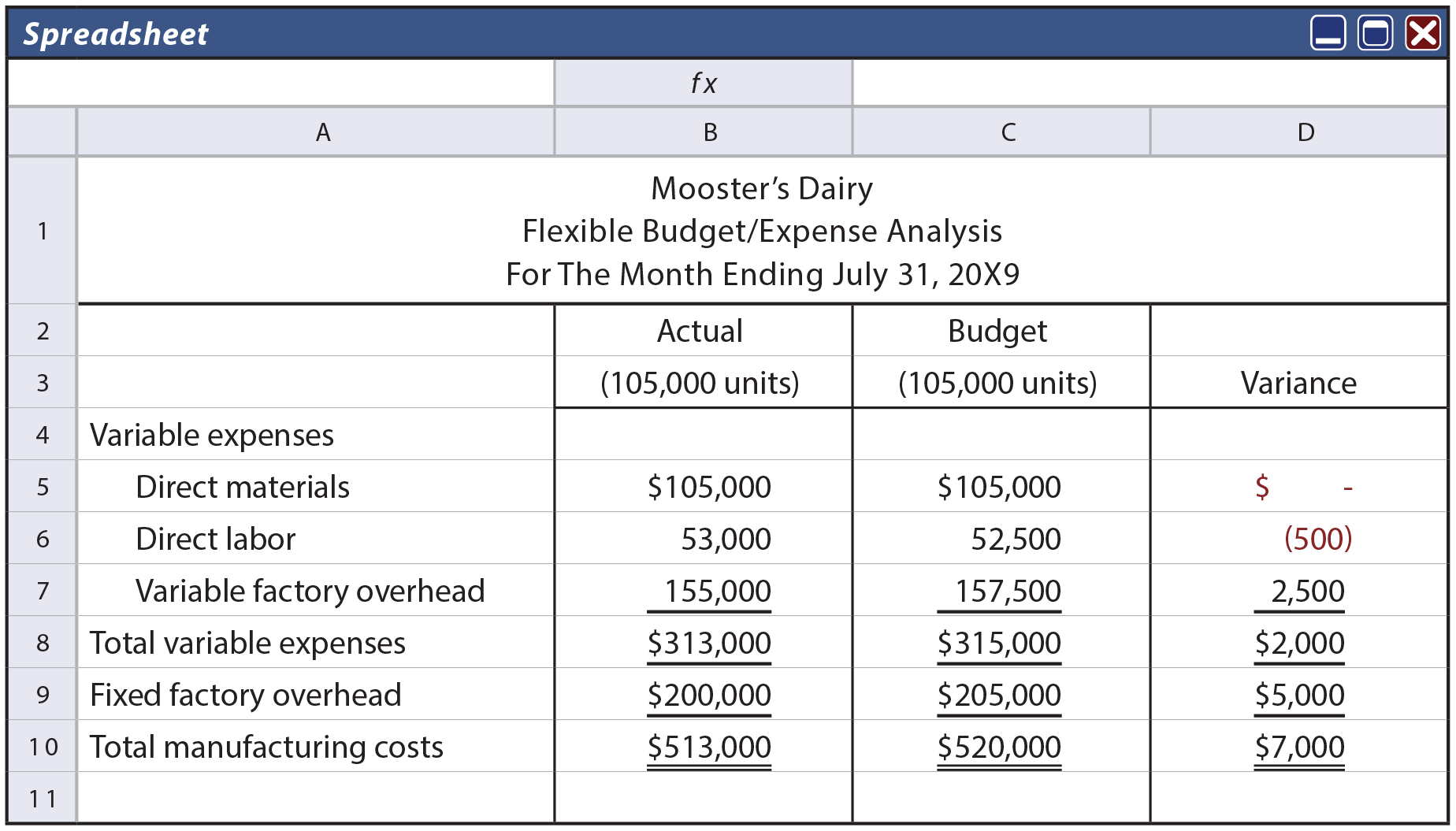

July of 20X9 was hotter than usual, and Mooster found itself actually producing 105,000 gallons. Total factory costs were $513,000. Mooster’s July budget versus actual expense analysis reveals unfavorable variances for materials, labor, and variable factory overhead. Does this mean the production manager has done a poor job in controlling costs? Remember that actual production volume exceeded plan. At a glance, it is challenging to reach any conclusion. What is needed is a performance report where the budget is “flexed” based on the actual volume.

The flexible budget reveals a much different picture. Rather than incurring $8,000 of cost overruns as portrayed by the variances associated with the static budget, one can see that total production costs were $7,000 below what would be expected at 105,000 units of output. On balance, it appears that the production manager has done a good job.

Specifically, direct materials cost exactly $1.00 per gallon of output. Direct labor totaled $500 in excess of the plan amount of $52,500 (105,000 units X $0.50 = $52,500), resulting in an unfavorable labor variance. This could be due to using more labor hours, paying a higher labor rate per hour, or some combination thereof. The variable factory overhead was expected at $157,500 (105,000 units X $1.50 per unit = $157,500), but actually cost only $155,000. Fixed factory overhead was $5,000 less than anticipated.

Evaluating Results

The flexible budget responds to changes in activity and generally provides a better tool for performance evaluation. It is driven by the expected cost behavior. Fixed factory overhead is the same no matter the activity level, and variable costs are a direct function of observed activity.

When performance evaluation is to be based on a static budget, there is very little incentive to drive sales and production above anticipated levels because increases in volume would tend to produce more costs and unfavorable variances. The flexible budget-based performance evaluation is a remedy for this phenomenon.

Planning

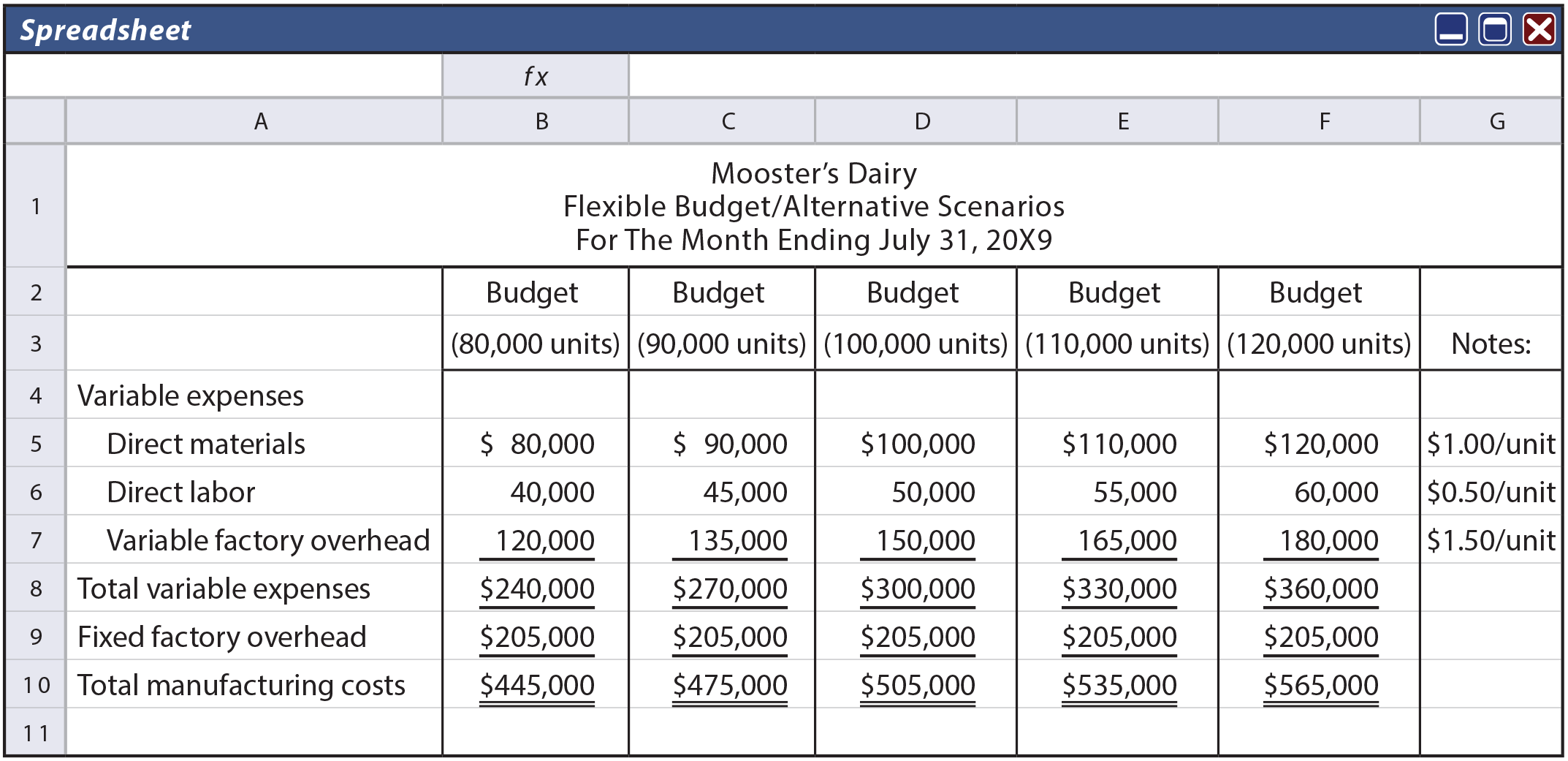

The flexible budget illustration for Mooster’s Dairy was prepared after actual production was known. While this tool is useful for performance evaluation, it does little to aid advance planning. But, flexible budgets can also be useful planning tools if prepared in advance. For instance, Mooster’s Dairy might anticipate alternative volumes based on temperature-related fluctuations in customer demand for ice cream. These fluctuations will be very important to managers as they plan daily staffing and purchases of milk and cream to support the manufacturing operation. As a result, Mooster’s Dairy might prepare an advance flexible budget based on many different scenarios.

The flexible budget illustration for Mooster’s Dairy was prepared after actual production was known. While this tool is useful for performance evaluation, it does little to aid advance planning. But, flexible budgets can also be useful planning tools if prepared in advance. For instance, Mooster’s Dairy might anticipate alternative volumes based on temperature-related fluctuations in customer demand for ice cream. These fluctuations will be very important to managers as they plan daily staffing and purchases of milk and cream to support the manufacturing operation. As a result, Mooster’s Dairy might prepare an advance flexible budget based on many different scenarios.

The following flexible budget reveals the expected aggregate expense levels. In reality, supporting flexible budget documents would resemble the comprehensive budget documents portrayed in the prior chapter. Such comprehensive documents would provide the information necessary to manage the smallest of operating details that must be adjusted as production volumes fluctuate.

Operating Efficiency

It perhaps goes without saying that computers are extremely helpful in preparing budget information that is easily flexed for changes in volume. Indeed, even the preparation of the very simple illustrative information for Mooster’s Dairy was aided by an electronic spreadsheet. Businesses save millions of dollars in accounting time by relying on computers to aid budget preparation.

It perhaps goes without saying that computers are extremely helpful in preparing budget information that is easily flexed for changes in volume. Indeed, even the preparation of the very simple illustrative information for Mooster’s Dairy was aided by an electronic spreadsheet. Businesses save millions of dollars in accounting time by relying on computers to aid budget preparation.

But, this savings is inconsequential when compared to the production efficiency and inventory savings that results from using computerized flexible budgeting tools. As production volumes ramp up and down to meet customer demand, computerized flexible budgets are adjusted on a real-time basis to send signals throughout today’s modern organization.

Selected information may also be shared with a business’s suppliers and customers via electronic data interchange. The net result is that the supply chain is immediately adjusted to match raw material orders to actual production needs, thereby eliminating billions of dollars of raw material waste and scrap.

| Did you learn? |

|---|

| Differentiate between a flexible budget and a static budget. |

| Be able to construct a flexible budget, and demonstrate how this interfaces with performance evaluation. |