The basic features of the accounting model in use today trace roots back over 500 years. Luca Pacioli, a Renaissance-era monk, developed a method for tracking the success or failure of trading ventures. The foundation of that system continues to serve the modern business world well, and is the entrenched cornerstone of even the most elaborate computerized systems. The nucleus of that system is the notion that a business entity can be described as a collection of assets and the corresponding claims against those assets. The claims can be divided into the claims of creditors and owners (i.e., liabilities and owners’ equity). This gives rise to the fundamental accounting equation:

Assets = Liabilities + Owners’ Equity

Assets

Assets are the economic resources of the entity, and include such items as cash, accounts receivable (amounts owed to a firm by its customers), inventories, land, buildings, equipment, and even intangible assets like patents and other legal rights. Assets entail probable future economic benefits to the owner.

Liabilities

Liabilities are amounts owed to others relating to loans, extensions of credit, and other obligations arising in the course of business. Implicit to the notion of a liability is the idea of an “existing” obligation to pay or perform some duty.

Owners’ Equity

Owners’ equity is the owner’s stake in the business. It is sometimes called net assets, because it is equivalent to assets minus liabilities for a particular business. Who are the “owners?” The answer to this question depends on the legal form of the entity; examples of entity types include sole proprietorships, partnerships, and corporations. A sole proprietorship is a business owned by one person, and its equity would typically consist of a single owner’s capital account. Conversely, a partnership is a business owned by more than one person, with its equity consisting of a separate capital account for each partner. Finally, a corporation is a very common entity form, with its ownership interest being represented by divisible units of ownership called shares of stock. Corporate shares are easily transferable, with the current holder(s) of the stock being the owners. The total owners’ equity (i.e., “stockholders’ equity”) of a corporation usually consists of several amounts, generally corresponding to the owner investments in the capital stock (by shareholders) and additional amounts generated through earnings that have not been paid out to shareholders as dividends (dividends are distributions to shareholders as a return on their investment). Earnings give rise to increases in retained earnings, while dividends (and losses) cause decreases.

Owners’ equity is the owner’s stake in the business. It is sometimes called net assets, because it is equivalent to assets minus liabilities for a particular business. Who are the “owners?” The answer to this question depends on the legal form of the entity; examples of entity types include sole proprietorships, partnerships, and corporations. A sole proprietorship is a business owned by one person, and its equity would typically consist of a single owner’s capital account. Conversely, a partnership is a business owned by more than one person, with its equity consisting of a separate capital account for each partner. Finally, a corporation is a very common entity form, with its ownership interest being represented by divisible units of ownership called shares of stock. Corporate shares are easily transferable, with the current holder(s) of the stock being the owners. The total owners’ equity (i.e., “stockholders’ equity”) of a corporation usually consists of several amounts, generally corresponding to the owner investments in the capital stock (by shareholders) and additional amounts generated through earnings that have not been paid out to shareholders as dividends (dividends are distributions to shareholders as a return on their investment). Earnings give rise to increases in retained earnings, while dividends (and losses) cause decreases.

Balance Sheet

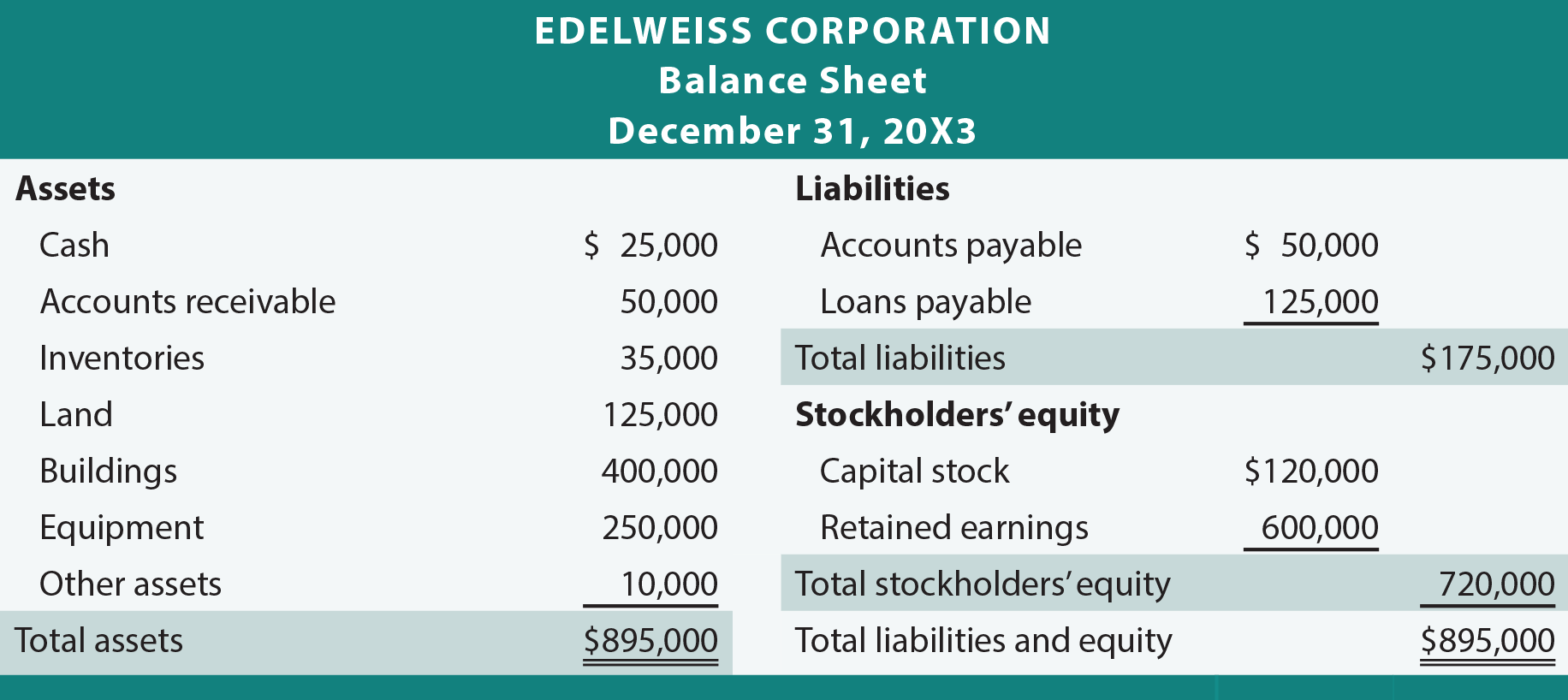

The accounting equation is the backbone of the accounting and reporting system. It is central to understanding a key financial statement known as the balance sheet (sometimes called the statement of financial position). The following illustration for Edelweiss Corporation shows a variety of assets that are reported at a total of $895,000. Creditors are owed $175,000, leaving $720,000 of stockholders’ equity. The stockholders’ equity section is divided into the $120,000 that was originally invested in Edelweiss Corporation by stockholders (i.e., capital stock), and the other $600,000 that was earned (and retained) by successful business performance over the life of the company.

Does the stockholders’ equity total mean the business is worth $720,000? No! Why not? Because many assets are not reported at current value. For example, although the land cost $125,000, Edelweiss Corporation’s balance sheet does not report its current worth. Similarly, the business may have unrecorded resources, such as a trade secret or a brand name that allows it to earn extraordinary profits. Alternatively, Edelweiss may be facing business risks or pending litigation that could limit its value. Consideration should be given to these important non-financial statement valuation issues if contemplating purchasing an investment in Edelweiss stock. This observation tells us that accounting statements are important in investment and credit decisions, but they are not the sole source of information for making investment and credit decisions.

Does the stockholders’ equity total mean the business is worth $720,000? No! Why not? Because many assets are not reported at current value. For example, although the land cost $125,000, Edelweiss Corporation’s balance sheet does not report its current worth. Similarly, the business may have unrecorded resources, such as a trade secret or a brand name that allows it to earn extraordinary profits. Alternatively, Edelweiss may be facing business risks or pending litigation that could limit its value. Consideration should be given to these important non-financial statement valuation issues if contemplating purchasing an investment in Edelweiss stock. This observation tells us that accounting statements are important in investment and credit decisions, but they are not the sole source of information for making investment and credit decisions.

Assets ($895,000) = Liabilities ($175,000) + Stockholders’ equity ($720,000)

Need help preparing for an exam?

Check out ExamCram the exam preparation tool!

| Did you learn? |

|---|

| Know the accounting equation, and mathematical variations of this equation (e.g., assets – liabilities = owner’s equity). |

| Define and cite examples of assets and liabilities. |

| What are three typical business entity forms? |

| Define retained earnings and identify the elements that cause it to change. |

| Show the relationship between the fundamental accounting equation and the structure of the balance sheet. |