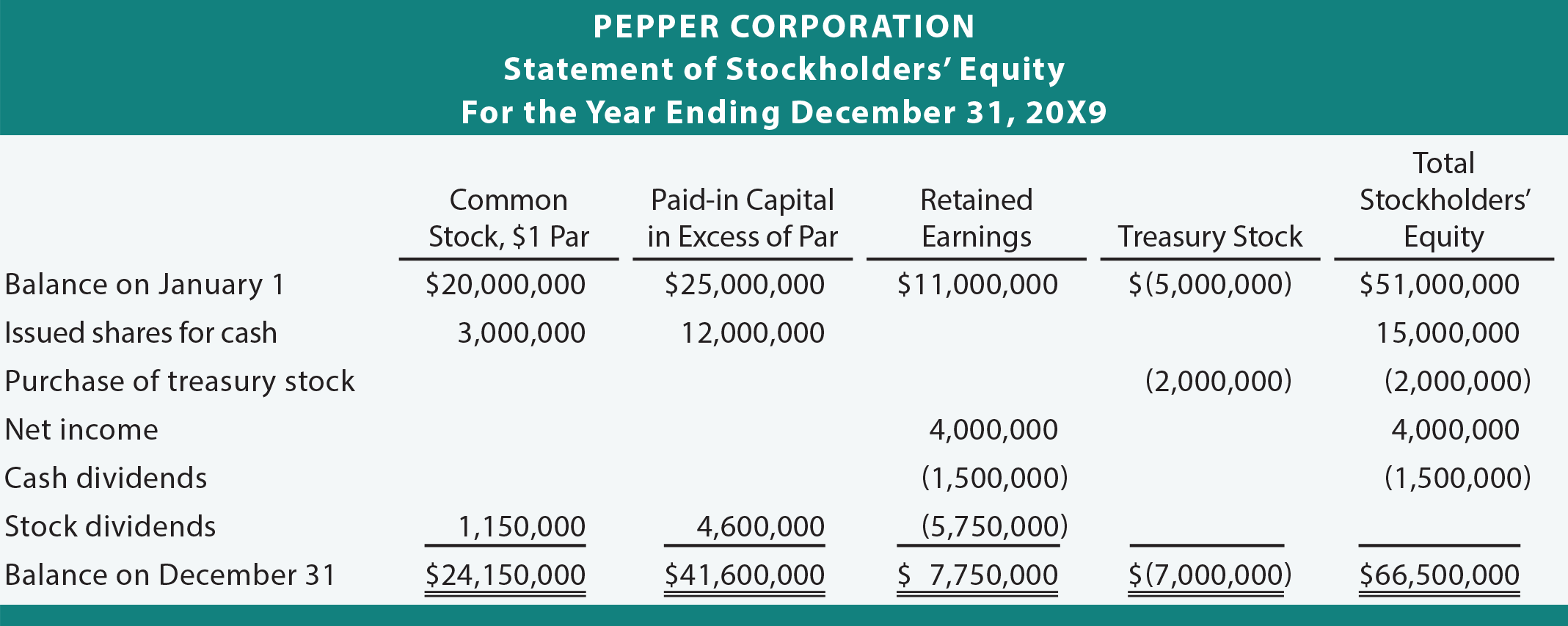

Remember that a company must present an income statement, balance sheet, statement of retained earnings, and statement of cash flows. However, it is also necessary to present additional information about changes in other equity accounts. This may be done by notes to the financial statements or other separate schedules. However, most companies will find it preferable to simply combine the required statement of retained earnings and information about changes in other equity accounts into a single statement of stockholders’ equity. Following is an example of such a statement.

Note that the company had several equity transactions during the year, and the retained earnings column corresponds to a statement of retained earnings. Companies may expand this presentation to include comparative data for multiple years. Under international reporting guidelines, the preceding statement is sometimes replaced by a statement of recognized income and expense that includes additional adjustments for allowed asset revaluations (“surpluses”). This format is usually supplemented by additional explanatory notes about changes in other equity accounts.

| Did you learn? |

|---|

| Be able to prepare a statement of stockholders’ equity. |

| Know about the international approach of presenting a statement of recognized income and expense. |

| Know about the international approach of adjusting equity for asset revaluations. |