Various reporting methods can be employed to facilitate managerial decision making. Consider that the same internal data can be generated and displayed in many ways. There is not a single correct method for “slicing and dicing” a company’s overall results into unitized information sets. And, there is no reason to think that a manager should be forced to make decisions based upon a single display of data. Modern information systems empower managers to look at the same data from multiple perspectives, and good managers will avail themselves of these tools as they consider data and make decisions.

Case Study

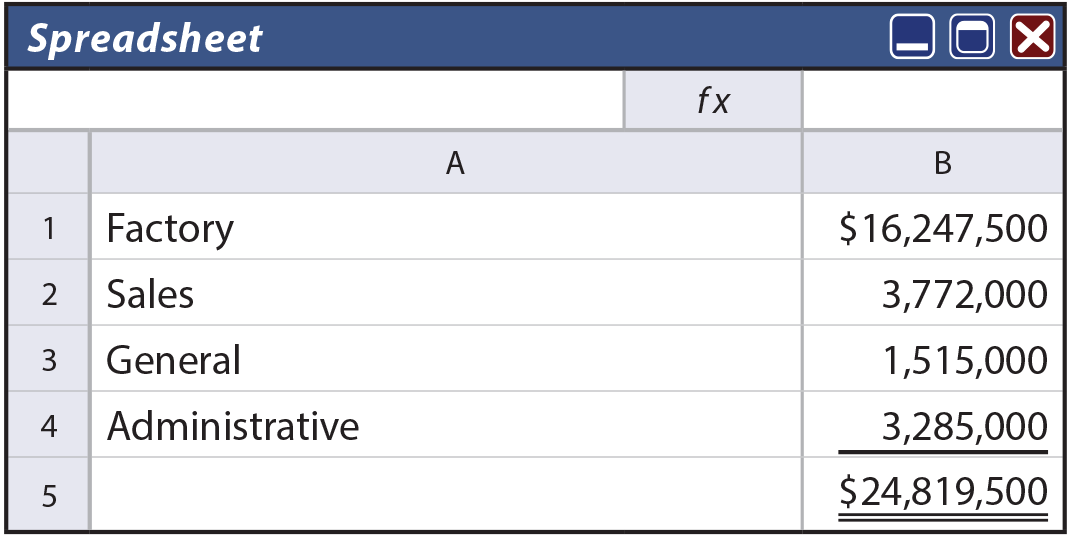

Consider the accompanying data set revealing that $24,819,500 was spent on compensation. Of that amount, $16,247,500 was spent on factory labor, and so forth. Each line item corresponds to an employee grouping, and those lines roughly relate to the individual categories that would be compiled in developing an overall income statement. Suppose the manager for this business is charged with reducing total compensation costs to $24,000,000. Which category should be cut? Would it be wise to cut each category in equal proportion to “spread the pain?” Is there a better way? Indeed, it is difficult to say by reviewing the data from a single perspective.

Consider the accompanying data set revealing that $24,819,500 was spent on compensation. Of that amount, $16,247,500 was spent on factory labor, and so forth. Each line item corresponds to an employee grouping, and those lines roughly relate to the individual categories that would be compiled in developing an overall income statement. Suppose the manager for this business is charged with reducing total compensation costs to $24,000,000. Which category should be cut? Would it be wise to cut each category in equal proportion to “spread the pain?” Is there a better way? Indeed, it is difficult to say by reviewing the data from a single perspective.

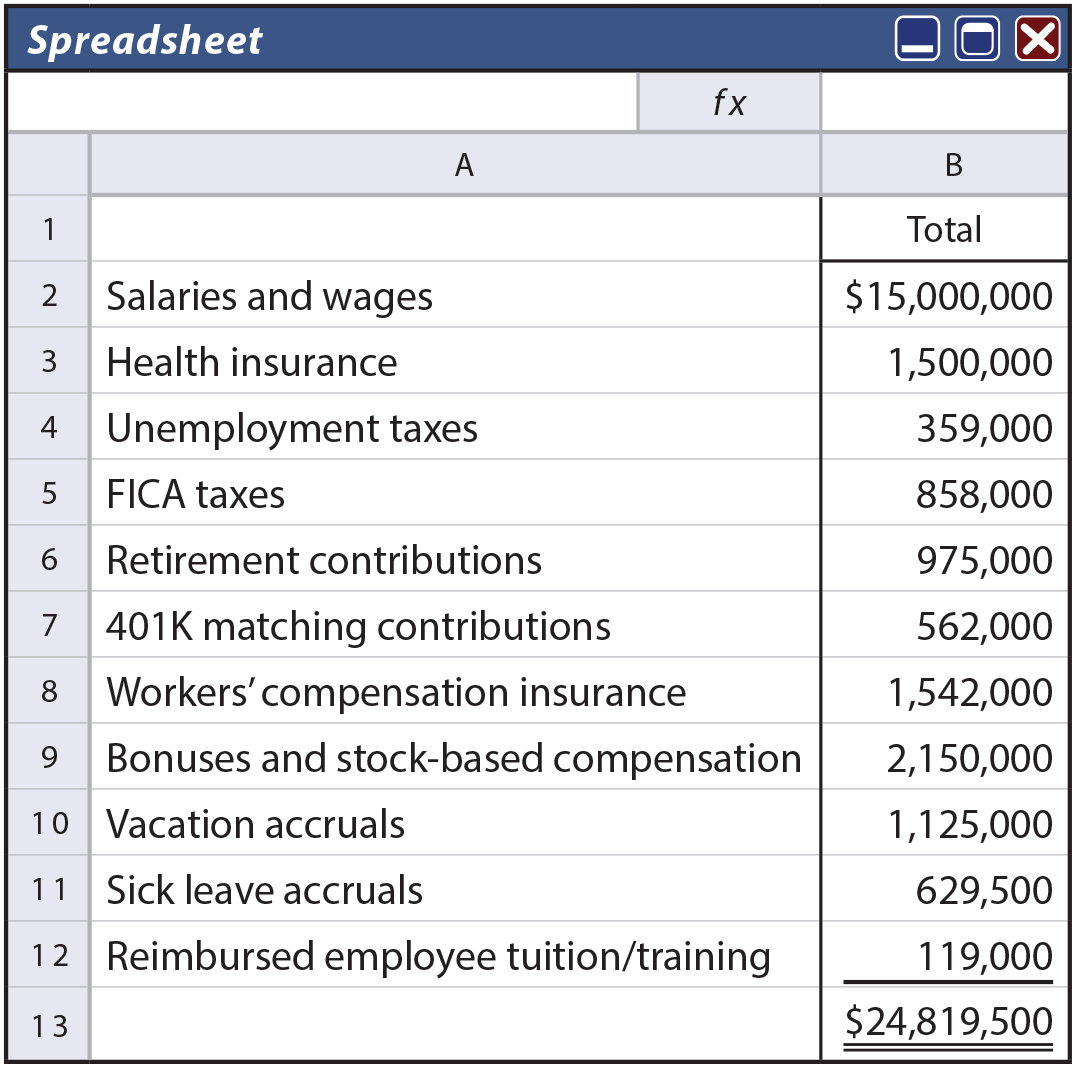

The same data can be rearranged in a different fashion. Rather than sorting the $24,819,500 into typical financial statement line-item expense categories, it can instead be presented by object of expenditure. Object of expenditures would relate to categories such as salaries and wages, insurance, and so forth. Here, it can be seen that the same total cost of $24,819,500 is distributed to match the object of expenditure.

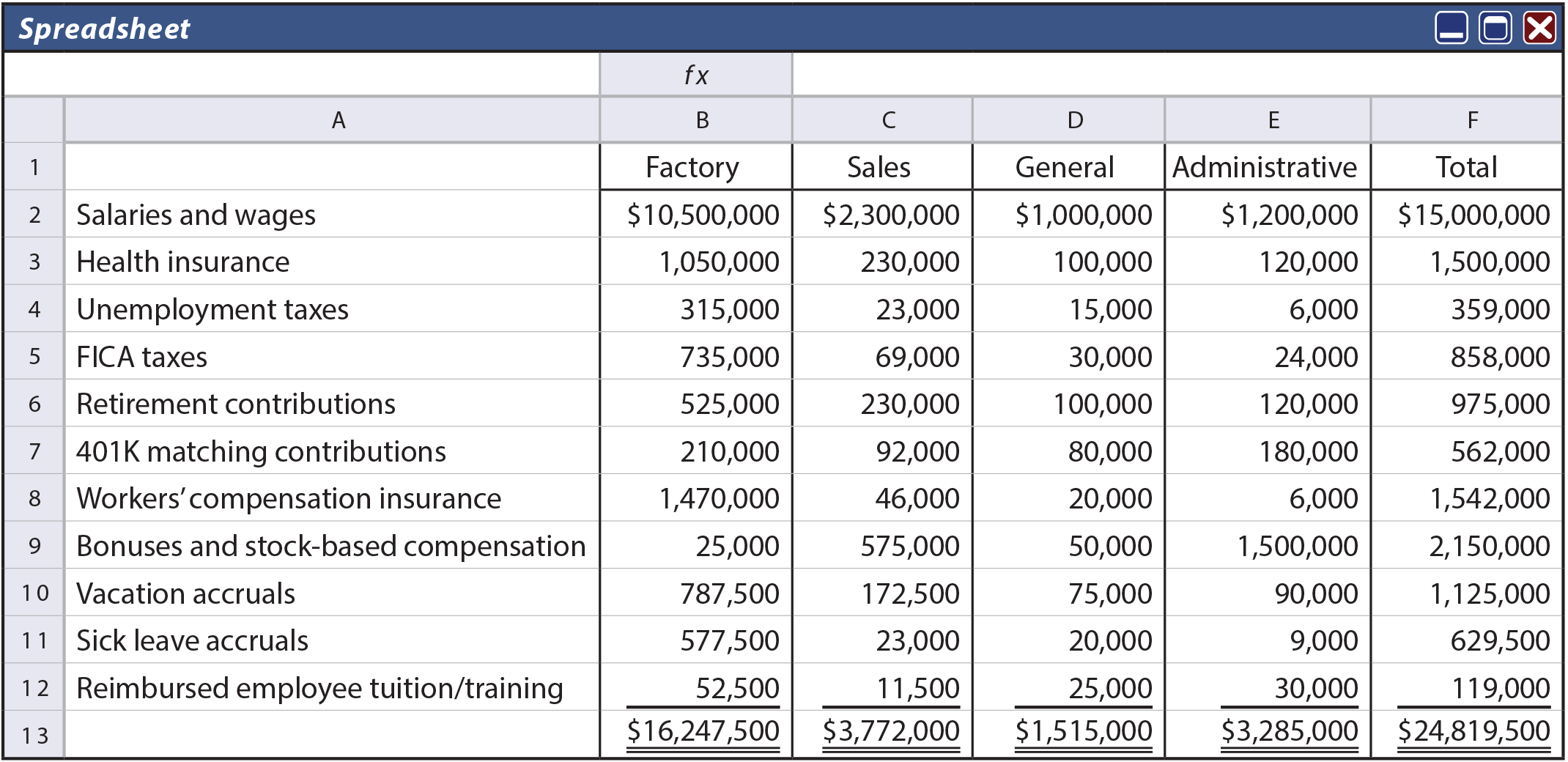

Perhaps the revised display provides added insight into cost control opportunities. Some specific expenditure category might be targeted for reduction if it is viewed as discretionary or not critical to the productive mission of the entity. The data might be further arranged into an even more detailed matrix format for closer inspection, as shown in the following spreadsheet:

The column totals correspond to the information in the first report, and the row totals correspond to the information in the second report. The individual cells within the matrix bring attention to a number of areas where added cost control might be effectively implemented. For instance, workers’ compensation insurance for factory labor is $1,470,000. Perhaps a different insurance carrier might provide a better rate for this coverage, contributing a significant portion of the targeted overall cost reduction. Or, maybe the bonus plan for administrative staff ($1,500,000) should be targeted; perhaps this category is in “runaway mode” since it exceeds the base amount for administrative salaries. Examine the data and identify other areas that offer potential cost reduction.

The key point is that managers should be prepared to consider alternative or expanded data sets as they contemplate difficult decisions. Viewing data only by line item or only by object of expenditure can greatly limit insight into business operations. Today’s accounting systems enable organizing and rearranging data sets with relative ease. These systems can be costly to design and implement, but they can pay great returns when managers take advantage of the robust information they are capable of producing.

Business Dashboard

A rapidly growing trend is for business managers to utilize dashboards to monitor information on a real-time basis. Business dashboards present corporate information on personal computers. The information is constantly updated to reflect the latest developments, much like a car’s dashboard reflects current speed, water temperature, oil pressure, and so forth. Following is a screenshot of a sample business dashboard:

Dashboards are easily customized by each manager. Personalized dashboards can easily be set up that are specifically tailored to the information needs of a sales manager, CFO, or other decision maker. Typically, specific line items on a dashboard can be “clicked” to open windows of additional data in support of the key metrics displayed. An important feature of a business dashboard is secure internet access so that an on-the-go executive always has critical information readily available.

Big Data

Modern information systems have enabled the accumulation and storage of massive amounts of data (“data warehousing”) about not only transaction amounts, but numerous other related attributes. The resulting big data essentially contain the kernels of information necessary to answer questions about the “who, what, when, where, and why” of all business activity.

It is said that knowledge is power. People tend to buy less toilet paper in the three months leading up to a planned home sale. How powerful is this information to a realtor in pursuit of potential clients? Fraudulent CFOs tend to post errant entries late at night. Does this help the auditor zero in on rogue behavior? The key to knowledge, and therefore power (and profit), is to be able to successfully mine and analyze vast data sets, thereby converting seemingly endless random points into a connected set of useful information. The field of accountancy, and therefore the core competencies of aspiring accountants, is rapidly expanding to include skills in data analytics and statistics.

| Did you learn? |

|---|

| Distinguish between line item and object of expenditure presentations of data. |

| Know how management can use line item data. |

| Know how management can use object of expenditure data. |